All Categories

Featured

Table of Contents

The are whole life insurance policy and universal life insurance. The money worth is not included to the death advantage.

The policy car loan passion price is 6%. Going this route, the passion he pays goes back right into his plan's cash money value instead of a financial establishment.

Picture never ever having to fret about financial institution car loans or high interest rates again. That's the power of unlimited financial life insurance coverage.

There's no set financing term, and you have the liberty to pick the repayment timetable, which can be as leisurely as settling the lending at the time of fatality. This versatility includes the servicing of the finances, where you can decide for interest-only repayments, maintaining the loan equilibrium flat and workable.

Holding money in an IUL dealt with account being credited rate of interest can frequently be much better than holding the cash money on deposit at a bank.: You've constantly dreamed of opening your own bakery. You can obtain from your IUL plan to cover the preliminary expenditures of renting out a space, buying equipment, and hiring personnel.

Be Your Own Banker Concept

Personal financings can be obtained from traditional financial institutions and credit unions. Obtaining money on a credit scores card is normally very expensive with yearly portion prices of interest (APR) frequently reaching 20% to 30% or more a year.

The tax obligation therapy of plan fundings can differ dramatically depending on your nation of home and the certain regards to your IUL policy. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, policy car loans are normally tax-free, providing a significant benefit. Nonetheless, in various other territories, there may be tax implications to take into consideration, such as potential tax obligations on the lending.

Term life insurance only provides a fatality benefit, without any money value build-up. This indicates there's no money worth to borrow versus.

Whole Life Insurance As A Bank

When you initially hear concerning the Infinite Financial Principle (IBC), your first response could be: This seems too great to be real. The problem with the Infinite Banking Principle is not the idea yet those persons providing an unfavorable review of Infinite Financial as a principle.

As IBC Authorized Practitioners through the Nelson Nash Institute, we assumed we would respond to some of the top questions individuals search for online when finding out and understanding everything to do with the Infinite Financial Concept. So, what is Infinite Banking? Infinite Banking was created by Nelson Nash in 2000 and fully clarified with the magazine of his publication Becoming Your Own Banker: Open the Infinite Financial Concept.

Be My Own Bank

You believe you are coming out financially in advance because you pay no rate of interest, yet you are not. With saving and paying cash money, you might not pay interest, yet you are utilizing your cash as soon as; when you invest it, it's gone for life, and you provide up on the opportunity to gain lifetime compound interest on that cash.

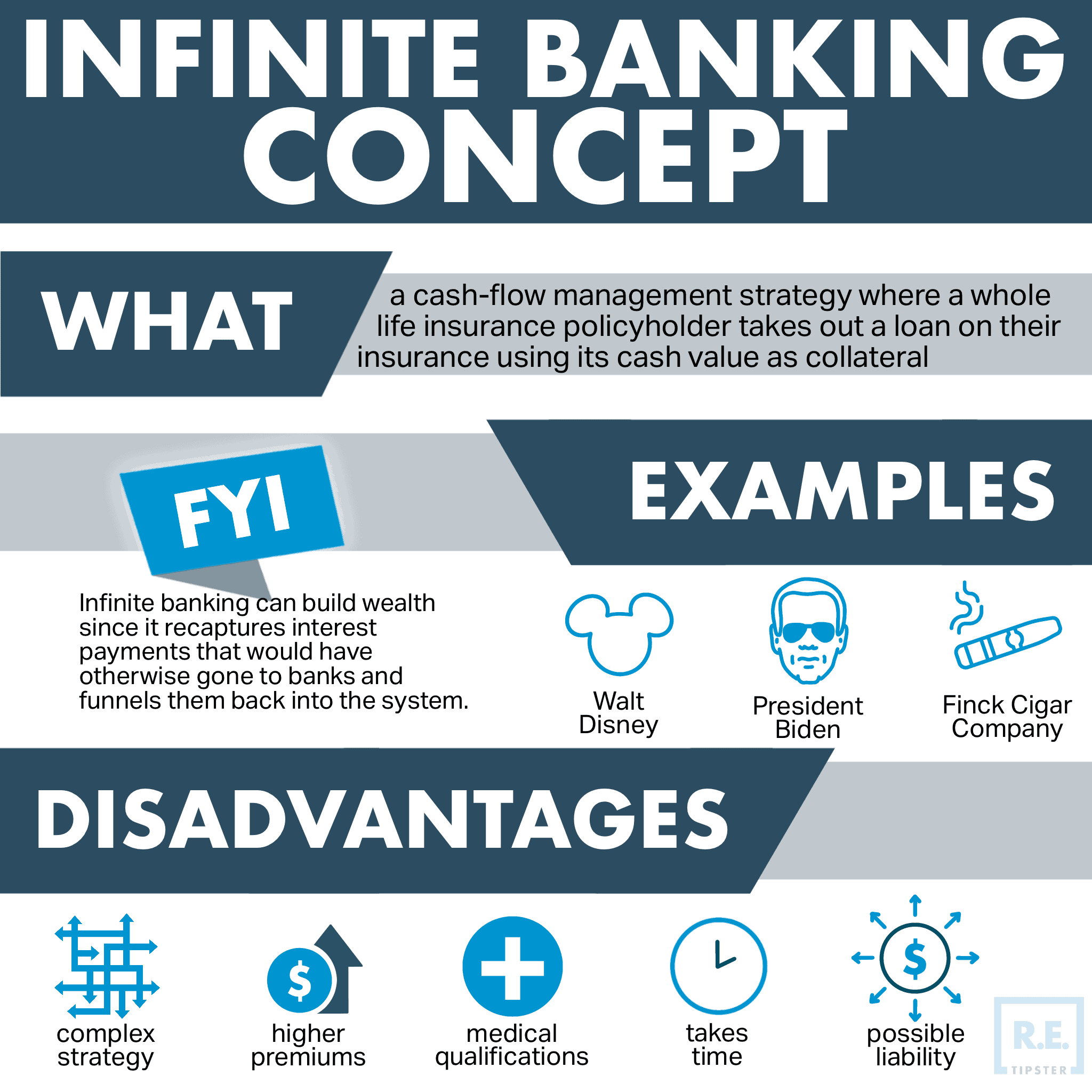

Billionaires such as Walt Disney, the Rockefeller family members and Jim Pattison have leveraged the residential properties of entire life insurance policy that dates back 174 years. Also financial institutions use whole life insurance coverage for the exact same objectives. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Revenue Agency (CRA) also identifies the value of participating entire life insurance policy as an unique asset class utilized to produce lasting equity securely and naturally and provide tax benefits outside the scope of standard investments.

How Do I Become My Own Bank

It permits you to create riches by satisfying the financial function in your very own life and the capability to self-finance significant way of life purchases and costs without disrupting the compound interest. One of the simplest means to believe concerning an IBC-type taking part entire life insurance policy plan is it is equivalent to paying a home loan on a home.

In time, this would certainly create a "constant compounding" result. You understand! When you obtain from your getting involved entire life insurance policy plan, the cash money worth proceeds to grow nonstop as if you never ever obtained from it to begin with. This is due to the fact that you are using the money worth and survivor benefit as collateral for a finance from the life insurance firm or as collateral from a third-party loan provider (referred to as collateral financing).

That's why it's critical to deal with a Licensed Life Insurance Broker authorized in Infinite Financial who structures your participating entire life insurance policy policy correctly so you can stay clear of unfavorable tax implications. Infinite Banking as a financial approach is not for everyone. Below are several of the advantages and disadvantages of Infinite Financial you should seriously think about in making a decision whether to progress.

Our favored insurance coverage service provider, Equitable Life of Canada, a common life insurance business, concentrates on taking part entire life insurance policy plans details to Infinite Banking. Also, in a shared life insurance policy firm, insurance holders are taken into consideration business co-owners and obtain a share of the divisible surplus created annually via dividends. We have a variety of carriers to select from, such as Canada Life, Manulife and Sun Lifedepending on the needs of our customers.

Please also download our 5 Top Inquiries to Ask A Boundless Financial Agent Before You Employ Them. To find out more about Infinite Financial see: Please note: The product supplied in this e-newsletter is for educational and/or instructional functions only. The information, point of views and/or views shared in this e-newsletter are those of the authors and not always those of the representative.

Banking Life

The concept of Infinite Banking was produced by Nelson Nash in the 1980s. Nash was a finance professional and follower of the Austrian institution of business economics, which advocates that the worth of items aren't clearly the outcome of conventional financial frameworks like supply and demand. Rather, individuals value money and products in different ways based on their financial standing and needs.

One of the mistakes of typical banking, according to Nash, was high-interest prices on finances. Too several individuals, himself consisted of, obtained right into economic difficulty due to reliance on banking organizations.

Infinite Banking needs you to possess your monetary future. For goal-oriented individuals, it can be the ideal financial device ever before. Below are the advantages of Infinite Banking: Probably the single most helpful aspect of Infinite Financial is that it boosts your cash money circulation.

Dividend-paying whole life insurance is really reduced risk and provides you, the insurance holder, an excellent offer of control. The control that Infinite Financial offers can best be organized into two groups: tax obligation benefits and asset protections.

Whole life insurance policies are non-correlated properties. This is why they function so well as the financial structure of Infinite Financial. Despite what happens out there (stock, property, or otherwise), your insurance plan preserves its worth. Way too many people are missing this vital volatility buffer that aids protect and expand wide range, instead breaking their cash into 2 containers: financial institution accounts and investments.

Market-based financial investments expand riches much quicker but are exposed to market fluctuations, making them inherently risky. Suppose there were a 3rd bucket that supplied security however also moderate, surefire returns? Entire life insurance is that third container. Not only is the rate of return on your entire life insurance plan assured, your survivor benefit and premiums are likewise assured.

Becoming Your Own Banker Nelson Nash Pdf

Infinite Financial appeals to those looking for better financial control. Tax effectiveness: The money value grows tax-deferred, and plan car loans are tax-free, making it a tax-efficient tool for constructing riches.

Possession protection: In many states, the money worth of life insurance coverage is protected from financial institutions, including an additional layer of economic safety and security. While Infinite Banking has its benefits, it isn't a one-size-fits-all remedy, and it includes significant disadvantages. Below's why it might not be the most effective strategy: Infinite Banking typically calls for complex plan structuring, which can perplex insurance policy holders.

{kind=link}

Latest Posts

Bank On Yourself: Safe Money & Retirement Savings Strategies

Unlocking Wealth: Can You Use Life Insurance As A Bank?

Infinite Banking Concept Canada